From 2021 Semiconductor Shortages to Global Chip Glut

Microchip Supply Shortage

Bring up logistics and supply chains at a social gathering and you’ll probably notice people around you discovering they have somewhere else to be. It may not be a fun party topic but it’s no exaggeration that global supply chains are the arteries of civilization. Nationwide restaurant chains are just one of its smaller miracles. Modern advances in logistics and supply chain management are the reason you can rely on getting the same burger at an Applebee’s in Springfield, MO as you’d find at Applebees in Springfield, MA or even Springfield, IL. But mediocre burgers aren’t the only things benefiting from modern supply chains. It’s helped reduce the cost of consumer goods while spreading commerce and relative affluence around the globe. But 2021 has exposed fundamental vulnerabilities in our global supply chains. While it's tempting to blame shortages across many industries on COVID-19, experts have said that our global supply chains may have already had some preexisting conditions.

Choke Point Theory

Supply chains have always been crucial to human well-being, even before they were capable of giving us homogeneous restaurant chains. They're so crucial in fact that their disruption has been a pillar of military tactics since long before Napoleon said: “An army marches on its stomach!”

The 20th century saw the evolution of a new branch of the United States military that would specialize in foiling enemy supply. Malcolm Gladwell’s recent book, Bomber Mafia covers this important chapter in American military history that sheds some light on the durability of past supply chains. A handful of World War One-veteran US Army officers, led by Brig.-Gen. William L. Mitchell (right), believed they had figured out the secret to winning wars with limited conventional battle. A groundbreaking Army Air Force doctrine was developed alongside new long-range bomber technology, both were ready for trial runs when the US entered World War Two.

The 20th century saw the evolution of a new branch of the United States military that would specialize in foiling enemy supply. Malcolm Gladwell’s recent book, Bomber Mafia covers this important chapter in American military history that sheds some light on the durability of past supply chains. A handful of World War One-veteran US Army officers, led by Brig.-Gen. William L. Mitchell (right), believed they had figured out the secret to winning wars with limited conventional battle. A groundbreaking Army Air Force doctrine was developed alongside new long-range bomber technology, both were ready for trial runs when the US entered World War Two.

The bold new idea for warfare of the 1940s was dubbed Industrial Choke Point Theory, and its proponents believed it could help America and its allies avoid the nastiness of World War One's trench warfare. The theory behind it was simple: Bring down specific choke point industries through precision daylight bombing, and you bring down the enemy nation’s military capability with fewer overall casualties.

The theory was exercised in October, 1943 when the US Army Air Force attacked factories around Schweinfurt, Bavaria in an attempt to relieve the Germans of one of its most important industrial choke points, ball bearings. It must have seemed like a brilliant idea at the time because ball bearings are the grease upon which machinery moves, including machines of war.

Sadly, US Army Intelligence underestimated German defences in the region and the resulting bloody air battle earned the tragic moniker "Black Thursday". Over 600 US airmen were killed and nearly every one of the 291 bombers that participated were damaged in the attack, 60 were lost and 17 more irreparably damaged. It's remembered as the worst single day for the US Army Air Force in World War Two, leaving Hitler to declare another great German victory. The bombing disabled an estimated 34% of German ball bearing production, but US Army Intelligence had overestimated the importance of the ball bearing plants to German manufacturing. The Germans had a highly flexible supply chain that included not only large stock piles of the critical material but plenty of alternate supply sources from the Swiss and Swedes ready to fill any gaps.

Ball bearings are still a critical manufacturing component in anything built to move, but 2021 has taught us that today we have a new critical industrial choke point for equipment that doesn’t involve moving parts. The microchip is to the 21st century what the ball bearing was to the 20th. Fortunately, for now at least, our current shortages don’t involve long-range bombers.

2021 Global Chip Shortage

By now we’ve all been affected in some way by today’s chip shortages. It’s causing new car shortages and making it difficult to get your hands on new high-powered GPUs at your local computer shop. Good luck finding somewhere to buy anything with Nvidia’s new GeForce RTX 30-series or the new game consoles by Microsoft or Sony. It’s also causing some scarcity in the audio/video industry, it's the reason we don’t see deep stocks of this year’s AV receivers and other A/V products hitting the market.

By now we’ve all been affected in some way by today’s chip shortages. It’s causing new car shortages and making it difficult to get your hands on new high-powered GPUs at your local computer shop. Good luck finding somewhere to buy anything with Nvidia’s new GeForce RTX 30-series or the new game consoles by Microsoft or Sony. It’s also causing some scarcity in the audio/video industry, it's the reason we don’t see deep stocks of this year’s AV receivers and other A/V products hitting the market.

Some segments of consumer electronics have largely escaped the shortages. When President Trump declared a trade war on China in 2018, many manufacturers had the foresight to stockpile certain supplies just before COVID-19. Smartphones have been protected from the brunt of the semiconductor shortages because the smaller, high-end chips they use make them premium customers to chip-makers like TSMC. But even smartphone manufacturers are not completely immune. Apple is expecting silicon supply to affect iPhone and iPad production in 2021. Analysts say that smartphone companies are likely to start experiencing the effects of the shortages, starting with smaller phone companies like Levono and HMD Global, even as Gartner analysts say that demand for smartphones and tablets has spiked 26% in 2021.

Multiple Factors

Exactly how the world came to its semiconductor shortage is not something that can be fully explained here. It's been described as a perfect storm of factors. Cancelled chip orders from auto manufacturers that didn't expect a market rebound so early in 2021 while shipping slowdowns due to labor shortages have left floating inventory waiting to get into ports around the world. These factors have caused material shortages in nearly every business from hardware stores to bubble tea shops. Dumb bad luck has also contributed with fires at two important Japanese chip-plants. An AKM plant burned in October, 2020 causing a shortage of DACs and other chips used in audio-video equipment. In March 2021 a fire devastated the Renesas Electronics factory compounding chip shortages for the auto industry. If all of this during the pandemic weren't enough, 13,000-feet and 221,000-tons of ship called Ever Given ran aground during a dust storm in the Suez Canal. For North Americans that's about double the size and weight of the Edmund Fitzgerald. Ever Given took out one of the most important global trade arteries for six days, long enough to push already precarious supply schedules back for months.

But despite all of these factors, some experts say they may have simply illuminated the fragility in our global supply chains. That fragility didn't exist in 1943 when Germany's ball bearing industry was able to withstand attacks from the world's largest air power in midst of history's worst global conflict.

But despite all of these factors, some experts say they may have simply illuminated the fragility in our global supply chains. That fragility didn't exist in 1943 when Germany's ball bearing industry was able to withstand attacks from the world's largest air power in midst of history's worst global conflict.

If 2020 was a very bad year, 2021 has been a year of learning. One lesson we've learned is how much the world relies on a free and independent Taiwan—no matter what John Cena says! The island democracy is an important part of the global chip trade and home to TSMC the world’s largest player in the semiconductor foundry market. TSMC's pure-play foundries are chip plants capable of fabricating the highest-end chips from other company’s designs. Trade restrictions on China cut America's use of China's biggest chip maker SMIC, and this only added more reliance on TSMC's already loaded capacity.

At least one of the root causes of our supply chain's susceptibility to shortages is an interesting story from another Asian island democracy, a close neighbor and ally of Taiwan.

Auto-Industry Supply Chain Crisis

Arguably, the industry hardest hit by the chip crisis has been the auto industry. But auto-manufacturing happens to be the industry that invented the advances in supply chain efficiency that may have led directly to our present shortages and it all started in the struggling post-war Japanese industrial centers.

Toyota Just-in-Time!

In the years after the second world war, Japan had a domestic automotive industry that found itself in competition with American automakers for a piece of the lucrative American market. But Japanese manufacturers had a problem competing with American manufacturers in economies of scale. American car companies had the luxury of devoting an entire assembly line to the production of just one vehicle and making it thousands of times in a process called batch manufacturing. Unfortunately for Japanese automakers like Toyota, the same scale just didn’t exist. Making cars was a slower, more expensive and overall less competitive process.

In the years after the second world war, Japan had a domestic automotive industry that found itself in competition with American automakers for a piece of the lucrative American market. But Japanese manufacturers had a problem competing with American manufacturers in economies of scale. American car companies had the luxury of devoting an entire assembly line to the production of just one vehicle and making it thousands of times in a process called batch manufacturing. Unfortunately for Japanese automakers like Toyota, the same scale just didn’t exist. Making cars was a slower, more expensive and overall less competitive process.

By the spring of 1950 Toyota was desperate and close to going out of business. But the company had started working on a system intended to make it more competitive, the Toyota Production System (TPS). Over time, Toyota’s system evolved with several hard technical innovations that brought broad efficiency to every step in manufacturing. But it also brought soft innovations with a corporate culture that valued workers ideas to bring adaptability to everyday challenges. It’s the enduring influence of TPS’s soft innovations that many large companies employ when they attempt to nurture a positive and open corporate culture.

But it's the TPS hard innovations that would go on to be even more influential worldwide in manufacturing and supply chain management. Toyota created a new method that most industries practice today, called Just In Time Manufacturing.

Just In Time is a system that emphasizes increased manufacturing efficiency while limiting waste. To grossly oversimplify, it overhauled manufacturing into a pull process rather than push. An auto part is only manufactured as needed by the next part in the production chain. Using the new method, parts arrive just in time to be used immediately in the parts requiring them. The result was a reduction in labor and warehouse space. By the early 1970s the new management philosophy was being perfected across Toyota's auto plants by Taiichi Ohno, widely considered the father of JiT. By the 1980s it had begun to spread worldwide to nearly every industry and it would become a cornerstone in the growing consumer electronics industry.

Industrial Judo

It should be no surprise that an industrial framework maximizing efficiency would be developed in Japan. It seems likely that Taiichi Ohno followed the mindset of the Judoka. Just in Time could be described as “minimal manufacturing for maximum orders”. Effectively, the applied wisdom of Kanō Jigorō, the Japanese martial artist that founded Judo. Like the 1950s Japanese auto industry, Jigorō was small in stature but worked to develop techniques to take down much larger opponents. Jigorō's guiding principle of Judo is:

It should be no surprise that an industrial framework maximizing efficiency would be developed in Japan. It seems likely that Taiichi Ohno followed the mindset of the Judoka. Just in Time could be described as “minimal manufacturing for maximum orders”. Effectively, the applied wisdom of Kanō Jigorō, the Japanese martial artist that founded Judo. Like the 1950s Japanese auto industry, Jigorō was small in stature but worked to develop techniques to take down much larger opponents. Jigorō's guiding principle of Judo is:

“Maximum efficiency with minimum effort.” - Kanō Jigorō (1860-1938) Founder of Judo.

There's a strong theory out there that Taiichi Ohno was applying the Japanese martial art in manufacturing, I

wasn't the first to learn about Toyota's JiT and think, Judo.

"...while it might be going a bridge too far to suggest that Kano was responsible for Toyota’s TPS, it is certainly clear that Taiichi Ohno (大野 耐 February 29, 1912 – May 28, 1990) would have been exposed to the National Physical Education System that was being practiced in Japan at that time. It’s ethos would have been firmly imprinted in every person undertaking formal education in Japan." - The Do of Kano's Judo

Toyota’s system would become standard operating procedure for manufacturing around the world, and the indispensable principle for the notoriously short product life cycles in the semiconductor industry.

Industries around the world may owe a debt of gratitude to Toyota for TPS, but perhaps the world should have taken into account the full measure of its system. The world hastily adopted the cost savings benefits, but largely failed to adopt the holistic approach to flexibility and resilience that are also part of TPS. Today, chip shortages have auto-manufacturers experiencing delays in fulfilling vehicle orders. But the one auto-manufacturer that had been least affected by global semiconductor shortages just happens to be... Toyota!

Lesson Learned for Toyota

TPS’s guiding principles involved the removal of excess inventory, but not complete removal of all inventory. Toyota learned this lesson after a 9.0 magnitude earthquake rocked Japan back in 2011. This was the earthquake and subsequent tidal wave responsible for the meltdowns at the Fukushima nuclear power plant. It was a national tragedy that shocked the world, but for Japanese industry it caused major stress to supply chains. In accordance with TPS, Toyota used the accident as a learning experience and conducted a major internal review, a forensic study of its supply chain shortages.

The resulting report identified semiconductor supply as a serious choke point for the rest of its operations. Toyota successfully employed its soft innovations by responding to the report and implementing new policies that included a two to six month supply of chips for its new vehicles. Just in Time adopted a Just in Case clause! Like the fabled Ant and Grasshopper, Toyota prepared for winter. Despite being the company that invented the art of running tight on supply, one Reuters headline from last May described Toyota as “unfazed” by the chip crisis and was ready when the auto industry began rebounding in 2021. That is, until August ‘21 when it too had finally succumbed to the ongoing chip shortages. The company announced that it would pull back as much as 40% on production in September.

Ending the Semiconductor Choke Point

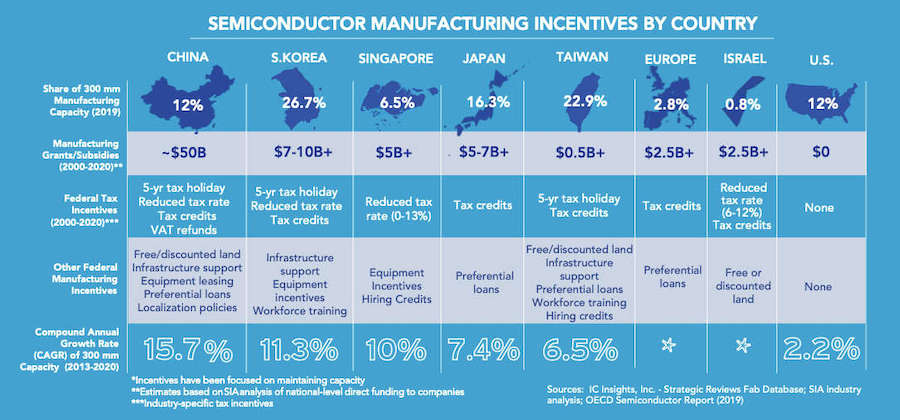

As the world seeks to counter the chip shortage, US President Joe Biden created an infrastructure plan that includes a $50-billion subsidy earmarked to reduce dependence on foreign-made chips. Two of the planet's biggest chip-makers, Samsung and TSMC agreed to commit billions of their own in investment for semiconductor plants on US soil. Samsung promises $17 billion on a new chip plant and looking into locations to build either in Arizona, New York or Texas. TSMC, the chip maker behind AMD, Nvidia and Apple announced that it would invest $10-$12 billion on a chip fabrication plant (or fab) capable of producing leading-edge 5-nm chips near Phoenix, Arizona. TSMC is even dangling further investment in 2nm chip technology at its Arizona plant sometime in the next 12 years. Meanwhile, American chip-maker, Intel plans to diversify its chip portfolio with

the creation of a new Intel Foundry Services (IFS) division.

That's a departure of Intel's business, it's better known as an IDM (Integrated Device Manufacturer), a company that manufactures chips of its own design. Negotiations may be underway for Intel to acquire GlobalFoundries for

some $30-billion, but Intel has also said it would devote $20-billion to

build two new foundries, also in Arizona.

As the world seeks to counter the chip shortage, US President Joe Biden created an infrastructure plan that includes a $50-billion subsidy earmarked to reduce dependence on foreign-made chips. Two of the planet's biggest chip-makers, Samsung and TSMC agreed to commit billions of their own in investment for semiconductor plants on US soil. Samsung promises $17 billion on a new chip plant and looking into locations to build either in Arizona, New York or Texas. TSMC, the chip maker behind AMD, Nvidia and Apple announced that it would invest $10-$12 billion on a chip fabrication plant (or fab) capable of producing leading-edge 5-nm chips near Phoenix, Arizona. TSMC is even dangling further investment in 2nm chip technology at its Arizona plant sometime in the next 12 years. Meanwhile, American chip-maker, Intel plans to diversify its chip portfolio with

the creation of a new Intel Foundry Services (IFS) division.

That's a departure of Intel's business, it's better known as an IDM (Integrated Device Manufacturer), a company that manufactures chips of its own design. Negotiations may be underway for Intel to acquire GlobalFoundries for

some $30-billion, but Intel has also said it would devote $20-billion to

build two new foundries, also in Arizona.

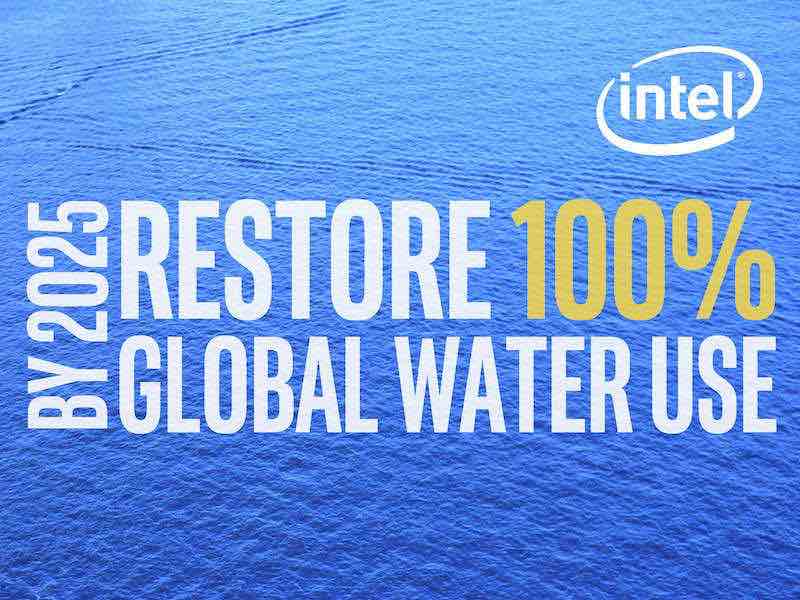

Water Foundries

Making semiconductors is thirsty business! TSMC has said its semiconductor manufacturing operations use about 156,000-tons of ultrapure water per-day. TSMC operates mostly in Taiwan, a country that has experienced water shortages in the past. So, how can Arizona handle such a dramatic uptick in water use? This is a state that only averages 13.6-inches of rainfall a year, less than half the national average of 30.3-inches. Intel is trying to help by making significant investment in what it calls "water foundries". The water used to clean wafers during chip manufacturing has to be specially purified to pass as ultrapure. That's water that is so pure, it's more acid than refreshing beverage, it's not what you crave on a hot day in the sun. Making ultrapure water is an important part of chip manufacturing and Intel is investing in 15 water restoration projects in Arizona capable of restoring 937-million gallons per-year back into the ecosystem. Once complete, this would make Intel's own Arizona operations a net-positive water consumer. Still, one has to wonder what makes Arizona so attractive to this industry when there are wetter states in the north with access to the Great Lakes.

Making semiconductors is thirsty business! TSMC has said its semiconductor manufacturing operations use about 156,000-tons of ultrapure water per-day. TSMC operates mostly in Taiwan, a country that has experienced water shortages in the past. So, how can Arizona handle such a dramatic uptick in water use? This is a state that only averages 13.6-inches of rainfall a year, less than half the national average of 30.3-inches. Intel is trying to help by making significant investment in what it calls "water foundries". The water used to clean wafers during chip manufacturing has to be specially purified to pass as ultrapure. That's water that is so pure, it's more acid than refreshing beverage, it's not what you crave on a hot day in the sun. Making ultrapure water is an important part of chip manufacturing and Intel is investing in 15 water restoration projects in Arizona capable of restoring 937-million gallons per-year back into the ecosystem. Once complete, this would make Intel's own Arizona operations a net-positive water consumer. Still, one has to wonder what makes Arizona so attractive to this industry when there are wetter states in the north with access to the Great Lakes.

USA would seem to have a bright future for domestic semiconductor manufacturing and new foundries with giants TSMC, Samsung and even Intel behind it. But with the rest of the world making similar investments, is it possible we have too many incoming chips? The analysts agree, IDC (International Data Corporation) recently predicted industry oversupply as early as 2023! That seems a little early, but it doesn't take an industry analyst to see that a chip glut is definitely in the mail.

Semiconductors are a notoriously cyclic business and a market down-cycle brought on by oversupply might not bode well for the future of new US foundries. At least not without further subsidies from Uncle Sam.

Cyclic Nature of the Semiconductor Industry

A 2005 study published in the Journal of Policy Modeling concluded that most semiconductor down-cycles are triggered by surges in semiconductor inventory and fab capacity rather than lack of demand. Typically, too many chips reduce value and profit from fulfilling orders. For the semiconductor fabrication business this could possibly compromise investment in the next-gen chip plant.

I Am The Laws

I Am The Laws

Moore’s Law states:

The number of semiconductors on an integrated circuit doubles every two years.

We've all heard of Moore’s Law and that it’s held more or less true since the early days of semiconductors. But a much less well-known other law in the chip business has also remained relevant over the same period. It’s sometimes called Moore’s Second Law, or Rock’s Law. This law is about the supply-side for semiconductors, named for Arthur Rock, a venture capitalist known for his predictive early investments in both Intel and Apple. Rock’s Law states:

The cost of a semiconductor chip fabrication plant doubles every four years.

Examples of Rock’s Law in action: In the year 2000 a modern fab cost a billion dollars. TSMC’s latest N5 fab, built in 2020 and capable of producing leading-edge 5nm technology, cost about $17-billion. TSMC’s next-gen 3nm process fab is estimated to cost $19.6-billion. It's no wonder engineers devote as much time attempting to slow Rock’s Law as they do accelerating Moore’s.

A chip fabrication plant is a significant up-front investment that must be covered by future production. Meanwhile, as soon as a new facility produces its first chip, that investment has already begun to decline in value. Asianometry, a brilliant semiconductor YouTuber describes the economics of chip-making when he says:

“The fab construction cost is fixed, but the marginal cost of making another chip is basically nil, so you want to make and sell as many chips as possible to amortize out those fixed costs.”

Unless demand for the coming generations of chips grows in lock-step with the new chip plants capacity, the US and governments around the world may be in the process of subsidizing the next industry down-cycle. Worst-case scenario: Chip prices bottom-out along with the profitability of America’s new publicly funded investment. The resulting semiconductor down-cycle may extend the new chip plant’s reliance on even more subsidies, which could have been the unspoken plan all along. The international chip business is no stranger to regular government investment.

From the Semiconductor Industry Association (SIA):

The SIA wants to normalize government chip subsidies

Slow Down the Chip Glut

Most industries experiencing a glut in supply might hold-off on production to create enough scarcity for profitability to return. But the economics of semiconductor manufacturing requires plants to sell every chip they’re capable of making, even at razor thin margins. But the new American chip plants may be able to survive the next down-cycle. Samsung and TSMC are two of the biggest players in the chip business, both are so big that they tend to value market share over profit. So, they're apt to weather a brief down-cycle storm so as not to lose customers to a competitor. It’s a similar principle a retailer like Walmart might employ when it opens a new store and wants to redirect the local market share of shoppers. Walmart is liable to briefly sell underwear at lower prices than the local underwear boutiques downtown can match in order to convert the local boutique's customers. When the local businesses close their doors, Walmart wins. When semiconductors being fabricated lose enough value that a down-cycle occurs, it will be followed by a market correction. For smaller chip manufacturers, this could mean getting a knock at the door from a larger buyer that wants to absorb them, or they could just go out of business. The correction reduces supply, bringing back profitability and the remaining companies can then afford another massive up-front investment in their next chip fabrication plant.

The semiconductor companies coming to America should be able to survive the next down-cycle that is liable to be brought on by a global surge in supply, hopefully without spending your children’s future tax dollars. Because when it comes to surviving a semiconductor down-cycle and TSMC and Samsung, they are the one who knocks!

Wayde is a tech-writer and content marketing consultant in Canada s tech hub Waterloo, Ontario and Editorialist for Audioholics.com. He's a big hockey fan as you'd expect from a Canadian. Wayde is also US Army veteran, but his favorite title is just "Dad".

View full profile